Get in touch with us at info@nativecanadianrvmarine.ca

APPROVED TO EXPLORE

We make financing simple, fast, and stress-free. No matter your credit situation. We offer flexible options and quick approvals. We make it easy to start your next adventure sooner. Get Approved Today!

Learn How Credit Scores are Calculated

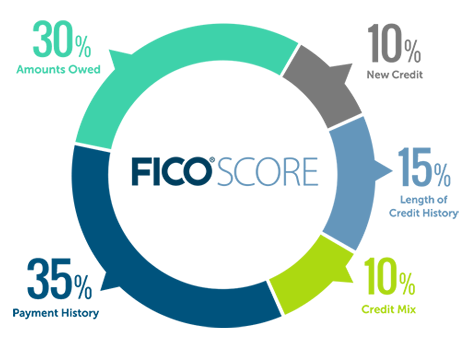

There is a lot of misinformation on how credit scores are calculated. Here’s what actually makes up your credit score.

FICO research has found that your level of debt is predictive of future credit performance because the amount owed typically impacts your ability to pay all monthly credit obligations on time. Not to worry if you have debt — it doesn’t automatically make you a high-risk borrower. However, as your balances increase so does the probability of difficulty meeting monthly payments on time, but that’s just part of what determines your credit score.

Part of the science of scoring is determining how much is too much for a given credit profile. Your FICO Scores take into account several factors.

Amounts owed on accounts determines 30% of a FICO® Score

What is Payment History?

Payment history shows how you’ve paid your accounts over the length of your credit. This evidence of repayment is the primary reason why payment history makes up 35% of your score and is a major factor in its calculation. Research shows that your track record of payment tends to be the strongest predictor of the likelihood that you’ll pay all debts as agreed to. And as you can imagine, a lender’s number one priority is your past record of paying back (or not) your loans.

A few late payments are not an automatic “score-killer.” An overall good credit history can outweigh one or two instances of late credit card payments.

However, having no late payments in your credit report doesn’t mean you’ll get a “perfect score.” Your payment history is just one piece of information used in calculating your FICO Scores.

What is the Length of your Credit History?

What is Credit Mix?

Even some people who haven’t had credit for a considerable length of time can still have a high FICO Score if the rest of their credit report looks good. A longer credit history will always have a positive effect on FICO Scores.

When it comes to length of credit history, your FICO Scores take three things into account:

-

How long your credit accounts have been open including the age of your oldest account, the age of your newest account, and an average age of all your accounts.

-

How long specific credit accounts have been open.

-

How long it has been since the account has been used.

So, what does it mean to you and your FICO Score? Creditors assess the risk of lending money through a variety of factors, one of them being your ability to successfully manage different types of credit. FICO not only looks at the mix of credit you have but also at the payment history of these credit types. For instance, if you have a great mix of installment and revolving loans, yet your payment history is bad, your FICO Score will reflect that negative payment history, which represents 35% of your FICO Score.

For creditors, it stands to reason that the better you manage different loans and lines of credit, the lower their risk when lending you money.

Again, since credit mix is only 10% of your FICO Score, it most likely won’t determine whether or not you obtain credit from lenders. However, if you’re striving to bring your FICO Score to the highest level it can be, your credit mix can play a part.

What is New Credit?

New Credit makes up 10% of a FICO Score. When you apply for new credit, inquiries remain on your credit report for 3 years. Fico Scores only consider inquires for the last 12 months.

People tend to have more credit today and shop for new credit more frequently than ever. FICO Scores reflect this reality. However, research shows that opening several new credit accounts in a short period of time represents greater risk – especially for people who don’t have a long credit history. Your FICO Scores take into account several factors when looking at new credit.

Here are the 3 things to look at for the new credit factor:

How many accounts you have.

Your FICO Scores look at how many new accounts you have by type of account. They may also look at how many of your accounts are new accounts. For creditors, it stands to reason that the better you manage different loans and lines of credit, the lower their risk when lending you money. Again, since credit mix is only 10% of your FICO Score, it most likely won’t determine whether or not you obtain credit from lenders. However, if you’re striving to bring your FICO Score to the highest level it can be, your credit mix can play a part.

Don't open new accounts too rapidly.

If you’ve been managing credit for a short time, don’t open a lot of new accounts too rapidly. New accounts will lower your average account age, which will have a larger effect on your FICO Scores if you don’t have a lot of other credit information. Even if you have used credit for a long time, opening a new account can still lower your FICO Scores.

How many recent inquiries you have

An inquiry is when a lender makes a request for your credit report or score. Although FICO Scores only consider inquiries from the last 12 months, inquiries remain on your credit report for two years. FICO Scores have been carefully designed to count only those inquiries that truly impact credit risk, as not all inquiries are related to credit risk.

There are 3 important faces about inquires to note:

-

Inquiries usually have a small impact

-

Many types of inquiries are ignored completely

-

The score allows for “rate shopping”

Remember: It's OK to request and check your own credit report.

Checking your credit report won’t affect your FICO Scores, as long as you order your credit report directly from the credit reporting agency or through an organization authorized to provide credit reports to consumers, such as myFICO.

How long it's been since you opened a new account.

This is the age of your most recently opened account. Your FICO Scores may consider the time that has passed since you opened a new credit account, for specific types of accounts.